## **How to Strategically Optimize Your Wage Loss Insurance Gross Er Potential**

The financial security of your household often rests on a single, vital pillar: your ability to earn a consistent income. When an unexpected illness or accident occurs, the sudden halt of that income can create a ripple effect of stress, debt, and uncertainty. Navigating the world of disability benefits and statutory accident schedules requires a deep understanding of how your earnings are calculated, particularly the distinction between net and gross figures. In the context of a **wage loss insurance gross er** strategy, the "gross" component is the most significant factor because it serves as the baseline for almost every calculation used by insurance adjusters. Whether you are a salaried professional, a freelance creator, or a small business owner, knowing how to leverage your gross earnings documentation can mean the difference between a payout that barely covers your rent and one that provides a true safety net. As we move through 2026, new legislative changes are shifting the burden of risk management onto the individual, making it more important than ever to be proactive about your coverage.

## **The Technical Mechanics of Gross Earnings in Wage Loss Claims**

To properly manage a **wage loss insurance gross er** claim, one must first master the technical definition of gross wages versus the "take-home" pay most people see on their bank statements. Gross wages represent the total compensation an employee earns before any deductions for taxes, healthcare premiums, or retirement contributions are removed. According to [Google](https://www.google.com/search?q=gross+wages+definition+for+insurance), this figure is the industry standard for calculating indemnity because it represents your total economic value to an employer. When an insurance company assesses a claim for lost income, they do not simply look at your last paycheck; they analyze your historical "gross er," or gross earnings, to establish an average weekly or monthly rate. For those in Ontario, this is often done using the OCF-2 Employer’s Confirmation Form, which requires a detailed breakdown of your earnings over the 52 weeks prior to the incident.

The calculation for self-employed individuals is significantly more complex. Rather than looking at a steady salary, insurers examine "Gross Income," which is defined as total revenue minus the cost of goods sold. As noted on [Wikipedia](https://en.wikipedia.org/wiki/Gross_income), this figure represents the core earning capacity of a business before operating expenses like rent, marketing, and utilities are subtracted. If you are a business owner, your **wage loss insurance gross er** benefit will depend heavily on your ability to produce clean profit and loss statements. If your personal income is intertwined with your business revenue, an insurer may require a "forensic accounting" approach to determine exactly how much personal income was lost due to your inability to work. Mastering these definitions ensures that you are not under-reporting your true income when it comes time to file a claim.

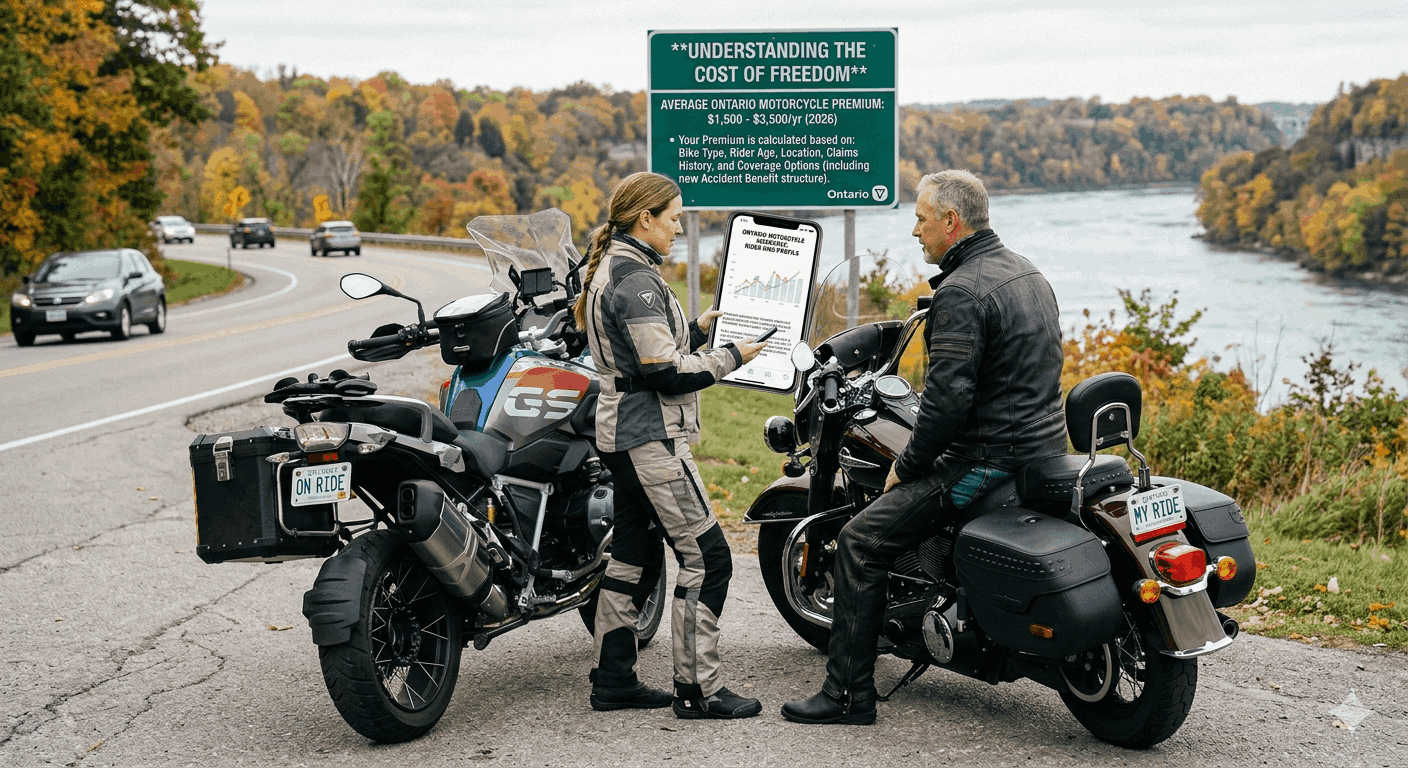

## **Navigating the 2026 Shift in Mandatory Accident Benefits**

A major transformation is currently underway in the insurance landscape, particularly for residents of Ontario. Starting July 1, 2026, the Statutory Accident Benefits Schedule (SABS) is moving from a mandatory "no-fault" model to a more flexible "optional" system. For decades, Income Replacement Benefits (IRB) were automatically included in every standard auto policy, providing up to $400 per week based on 70% of a claimant's gross earnings. However, according to recent updates from [Google News](https://www.google.com/search?q=Ontario+SABS+changes+July+2026), these benefits will now be optional. This means that if you do not explicitly "opt-in" and pay an additional premium, you will have zero automatic coverage for lost wages following a vehicle accident. This shift places a massive responsibility on consumers to act as their own risk managers.

For the high-earning professional, the standard $400 weekly limit has long been insufficient, as it only covers a gross annual income of approximately $30,000. In the new 2026 environment, it is highly recommended to purchase "optional" increases that can raise this benefit to $600, $800, or even $1,000 per week. Without these upgrades, a person earning a gross salary of $100,000 would face a devastating "income gap" if they were unable to work. Furthermore, the transition to an optional system may lead to an increase in "tort" lawsuits, where victims sue negligent drivers to recover the 30% of gross income not covered by standard benefits. Being aware of these legislative deadlines is crucial for ensuring your **wage loss insurance gross er** protections remain active and adequate.

## **Analytical Strategies for Maximizing Claim Payouts**

Maximizing a **wage loss insurance gross er** payout requires a professional and analytical approach to documentation. Insurers are naturally inclined to look for reasons to minimize their liability, often by excluding certain types of income from their calculations. To counter this, you must ensure that your "gross earnings" folder includes more than just base salary. You should document all bonuses, commissions, tips, and even employer-paid fringe benefits. According to [Forbes](https://www.google.com/search?q=https://www.forbes.com/advisor/business-insurance/disability-insurance/), many people fail to realize that commissions and overtime earned in the weeks prior to an accident can significantly "bump up" the average gross weekly income used for the benefit calculation. If your income is seasonal, you should advocate for an "apples-to-apples" comparison, asking the insurer to look at your earnings during the same peak period in previous years rather than a quiet off-season month.

Another vital strategy is the "dual-claim" approach. Many workers are covered by both a private Long-Term Disability (LTD) policy through their employer and a public system like Ontario's SABS or Canada's Employment Insurance (EI). It is important to understand "priority of payment" rules. Generally, if you are injured in a car accident, your auto insurer is the "first payer" for wage loss, but your private LTD policy can "top up" the difference to ensure you receive a higher percentage of your total gross earnings. However, be wary of "offsets," where one insurer reduces their payment based on what you receive from another. A professional insurance audit can help you identify these overlapping coverages and ensure you are not paying for redundant policies that cancel each other out during a crisis.

## **Conclusion and Your Personal Action Plan**

Securing your financial future through [**wage loss insurance gross er**](https://theaim.ca/business-interruption-insurance-comparing-the-forms-that-protect-your-business/) optimization is not a "set-and-forget" task. It requires a proactive commitment to understanding the math behind your policy and the laws governing your region. As the 2026 reforms approach, the safety net that many took for granted is becoming a series of choices that you must make today. By accurately documenting your total gross income, opting into the necessary benefit increases, and strategically coordinating your private and public coverages, you can build a fortress around your family's lifestyle. Don't wait for an accident to discover the gaps in your protection; your earning power is your most valuable asset, and it deserves professional-grade insurance.